The role of categorising in a couples budget: how it works

In brief:

- Categorising in a couples budget divides spending into fixed, variable and occasional costs for better insight. It reinforces behavioural change through emotionally labelled savings pots and automatic transfers. Regular reviews and clear agreements prevent money conflicts and create financial peace of mind.

Categorising in a couples budget means systematically sorting shared expenses into fixed categories to create financial clarity and equality. Without that structure, most couples have no idea where their money went by the end of the month. Good budget categorisation, such as the well-known 50/30/20 rule, divides net income into 50% fixed expenses, 30% personal wants and 20% savings or debt repayment. That structure gives you as a couple a fair and clear starting point. This article explains how categorisation works, why psychology plays a role in it and how to set it up practically.

How does the role of categorising in a couples budget help you understand your spending?

Categorising is meant to show you where money is going and to identify patterns — not primarily to cut costs. That distinction is significant. Once you divide your spending into groups, you immediately see which category is unexpectedly absorbing the most.

Within a couples budget there are three main groups:

- Fixed costs: rent or mortgage, insurance, subscriptions and energy bills. These costs are the same every month and easy to plan for.

- Variable costs: groceries, fuel, clothing and dining out. These fluctuate month to month and are where most money leaks occur.

- Occasional costs: birthday gifts, car repairs, holidays and annual premiums. Many couples forget this category entirely in their budget.

It is precisely that third group that causes surprises. Cash withdrawals and one-off annual expenses are often overlooked in budgets, making the overall picture unreliable. By labelling these costs too, you end up with a budget that reflects reality.

Periodic analysis strengthens the effect. Review together each month which category has gone over budget. That conversation takes ten minutes and delivers more value than a whole year of guessing where the money went.

Pro tip: Create a separate "unexpected" category with a fixed monthly amount, for example €50 to €100. That way you can absorb small surprises without throwing the budget off immediately.

What psychological factors play a role in categorising?

Mental accounting is the human tendency to treat money differently based on where it comes from or what it is intended for. Behavioural economist Richard Thaler described this principle and emphasised that using mental accounting deliberately demonstrably improves saving behaviour. For couples this means: give your savings pots a meaningful name.

A savings pot called "Dream Home" feels different from an account identified only by a number. Money that carries an emotional name is psychologically harder to spend on consumer purchases. That is no coincidence. Labelling money with names like "Italy Holiday" or "New Car" makes it less tempting to dip into that pot.

Loss aversion also comes into play. People find losing money twice as painful as gaining the same amount. Once you see a category in the red, it feels like a loss. That feeling motivates you to correct course far more than an abstract spreadsheet ever could.

"Consciously labelling money in categories and savings pots makes financial choices more tangible. Couples who do this experience less stress about money and make more deliberate decisions together."

Based on insights from Richard Thaler on mental accounting

Categorisation therefore works on two levels simultaneously. It gives you factual oversight and steers your behaviour in the right direction without you having to think about it consciously.

How do you set up categorisation practically in your couples budget?

A working system for categorising expenses does not need to be complicated. The most widely used method in the Netherlands — and the one most couples consider fair — is a combination of a joint account for fixed costs and individual accounts for personal spending, divided in proportion to income. Proportional division means: whoever earns more pays a larger share of the shared costs. That feels fairer than a rigid 50/50 split.

Here is how to set it up step by step:

- Map out all income. Note down both your net incomes, including any benefits or other income sources.

- Establish shared categories. Think about housing, transport, groceries, insurance and savings. Keep it to a maximum of eight categories to maintain clarity.

- Calculate each person's share. Use the income ratio to determine how much each person contributes to the joint account.

- Automate the transfers. Set up a direct debit for the day after payday. That way you no longer need to think about it.

- Evaluate monthly. Schedule a fixed moment — for example the first Sunday of the month — to go through the categories together.

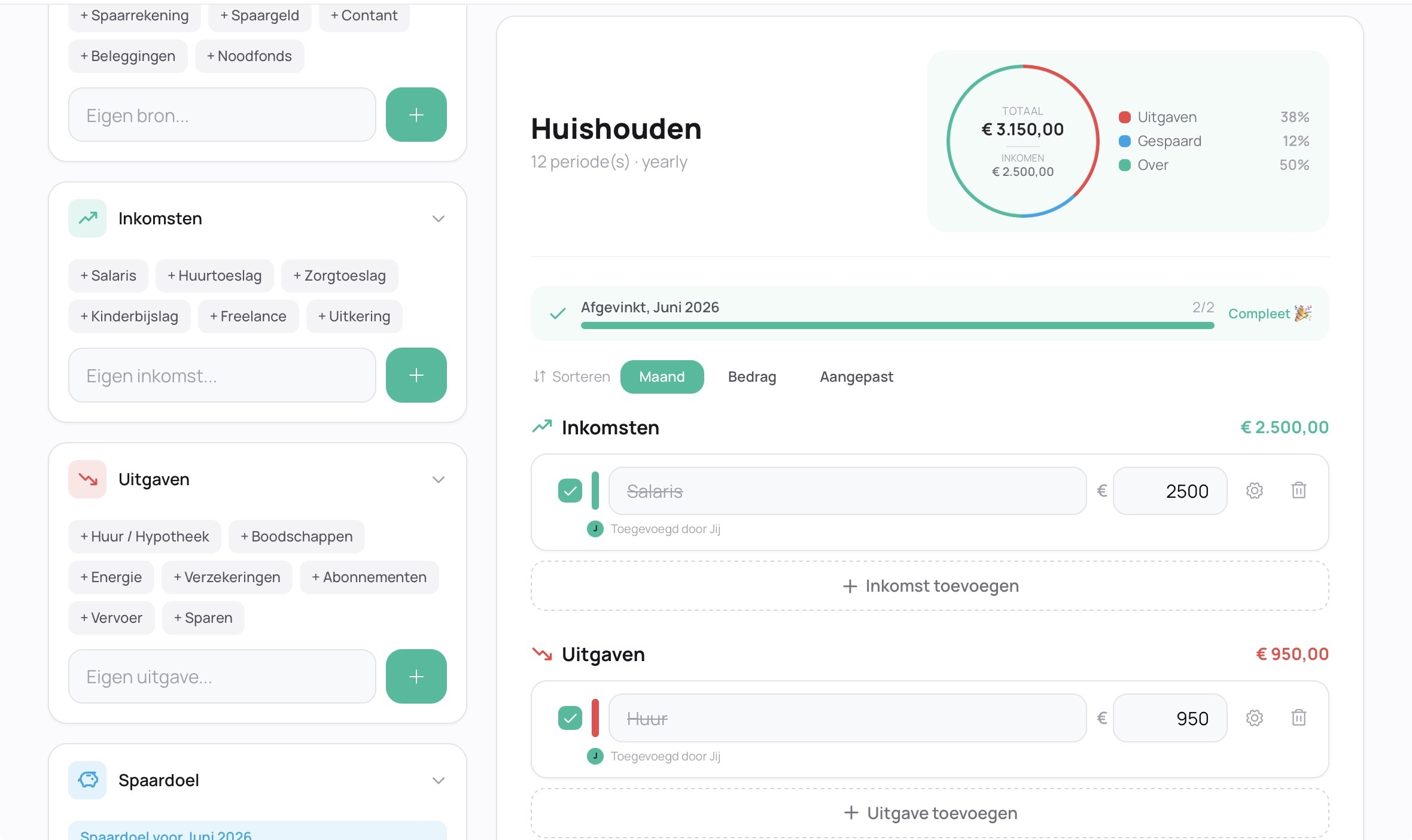

Digital tools make this process far less time-consuming. Budgivy offers a visual dashboard where you can see at a glance how each category is performing. The mobile Quick Add feature lets you enter expenses on the spot, so no receipt or reminder gets lost.

| Method | Suitable for | Point of attention |

|---|---|---|

| Joint account for everything | Couples with similar incomes | Less financial autonomy |

| Joint account for expenses, own account for personal spending | Couples with an income difference | Requires clear agreements |

| Fully separate with monthly reconciliation | Couples who have just moved in together | More administration |

Pro tip: Use the 50/30/20 rule as a starting point for your category breakdown. Then adjust the percentages to suit your own situation, because not every couple has the same fixed costs.

How does categorising prevent financial conflicts as a couple?

Money conflicts between couples rarely arise from a lack of money. They arise from a lack of clarity about what is shared and what is personal. Clear agreements about what is joint versus personal are the foundation of financial harmony. Without those agreements, frustration builds quietly until a small purchase turns into a big conversation.

Categorisation makes those agreements concrete. Once you decide together that "dining out" is a shared category but "clothing" is personal, the discussion about individual purchases disappears. The category is the agreement.

Transparency builds trust. Couples who can see each other's spending report less financial stress than those who cannot. Budgivy supports this with permission settings: you decide what the other person sees and what stays private. That gives freedom without secrets.

Circumstances change. A pregnancy, a new job or a move shifts the balance in your budget. That is why you should plan a longer review every six months to reassess the categories and the division. What worked last year may no longer apply this year.

Financial adviser Cinthia Zijderveld advises couples to approach financial discussions as a negotiation, not a conflict. That perspective removes the emotion and makes the conversation more productive.

- Agree on which expenses are always shared, such as rent and groceries.

- Set a personal "free to spend" amount per person, with no questions asked.

- Set a threshold for larger purchases that you discuss together — for example anything above €200.

- Review the agreements at least twice a year.

What is the impact of categorising on saving together?

Categorising structures saving and makes it measurable. Without a separate savings category, any money "left over" disappears into everyday spending. With a fixed savings category, you know every month exactly how much you are setting aside and what it is for.

Automation greatly amplifies this effect. Automating savings systems can increase the savings rate by up to three times, because it removes the reliance on willpower. That is a significant difference. Willpower is finite; an automatic transfer is not.

The psychological benefit of labelled savings goals makes it even more effective. A pot named "Kitchen Renovation 2027" motivates differently from an anonymous savings account. You watch the goal grow, which reinforces the behaviour of leaving it untouched.

Pro tip: Set the automatic savings transfer for the day after payday. That way you save first and live on what is left, rather than the other way round. Budgivy's savings plan feature supports this principle directly.

Categorisation also makes saving fairly distributed. If you are both saving towards the same goal, record who contributes how much and when the goal will be reached. That prevents disappointment if expectations turn out not to match afterwards.

Key takeaways

Categorising in a couples budget gives couples financial clarity, prevents conflicts and makes saving measurable by dividing spending into fixed groups and making agreements explicit.

| Point | Details |

|---|---|

| Categorising provides insight | Divide spending into fixed, variable and occasional costs to identify money leaks. |

| Psychology reinforces saving behaviour | Give savings pots emotional names to make it psychologically harder to empty them. |

| Proportional division is fairer | Whoever earns more pays a larger share of the shared costs. |

| Automation increases the savings rate | Automatic transfers after payday remove the reliance on willpower. |

| Clear agreements prevent conflicts | Establish what is shared and what is personal, and review this every six months. |

Why I see categorising as the foundation of every couples budget

After years of guiding couples through their finances, I keep seeing the same pattern. Couples who argue about money rarely argue about the money itself. They argue about uncertainty. Who pays for what? Why is there nothing left? Who spent that?

Categorisation solves that. Not because it eliminates every problem, but because it shifts the discussion from accusations to facts. You look together at a category that is in the red, not at each other.

What I see in practice is that couples who start categorising are often surprised by what they discover. The big expenses are not the problem. It is the small, recurring amounts that go unnoticed: streaming services nobody uses any more, subscriptions that renew automatically, coffee on the go that costs more per month than a weekend away.

My advice for couples who are just starting out: keep it simple. Begin with five categories. Only add more once you understand the system. A system that is too detailed is something nobody sticks with. A system that works is better than one that is perfect on paper.

Visual tools make the difference. Couples who can see their budget in a dashboard stick with it longer than couples working from a spreadsheet. That is not an opinion. That is what I see time and time again. Budgivy's budgeting approach aligns precisely with how people actually manage money in practice: visual, quick and without any hassle.

— Askin Aydin

Budgivy makes categorising simple for couples

You do not need to maintain a spreadsheet or compare bank statements to get a grip on your shared budget.

Budgivy is built as the anti-Excel alternative for couples who want to budget together without the hassle. In a matter of seconds you create a monthly budget, divide it into categories and immediately see where the money leaks are. The mobile Quick Add lets you enter expenses on the spot, the visual dashboard shows the status per category and the permission settings determine what you see together and what stays private. Smart Plans automatically provides advice based on the 50/30/20 rule, without adjusting any figures on its own. Start today with no account required at budgivy.app.

Frequently asked questions

What is categorising in a couples budget?

Categorising in a couples budget means dividing shared expenses into fixed groups, such as housing, groceries and savings. It gives couples immediate insight into where their money is going.

How do couples fairly distribute expenses across categories?

The most widely used method in the Netherlands is division in proportion to income. Whoever earns more contributes a larger share to the joint account for fixed costs.

Why does categorising help prevent money conflicts?

Categorisation makes agreements concrete. Couples who establish what is shared and what is personal have fewer discussions about individual purchases.

How often should couples review their budget categories?

A monthly ten-minute check is sufficient for day-to-day adjustments. In addition, schedule a longer review every six months to adapt the division and categories to changed circumstances.

Does automation make categorising easier?

Automating savings transfers and fixed payments removes the willpower that would otherwise be required. That demonstrably increases the savings rate and keeps the budget reliable without daily attention.

Recommendation

Create your first budget for free — no hassle, no spreadsheet.